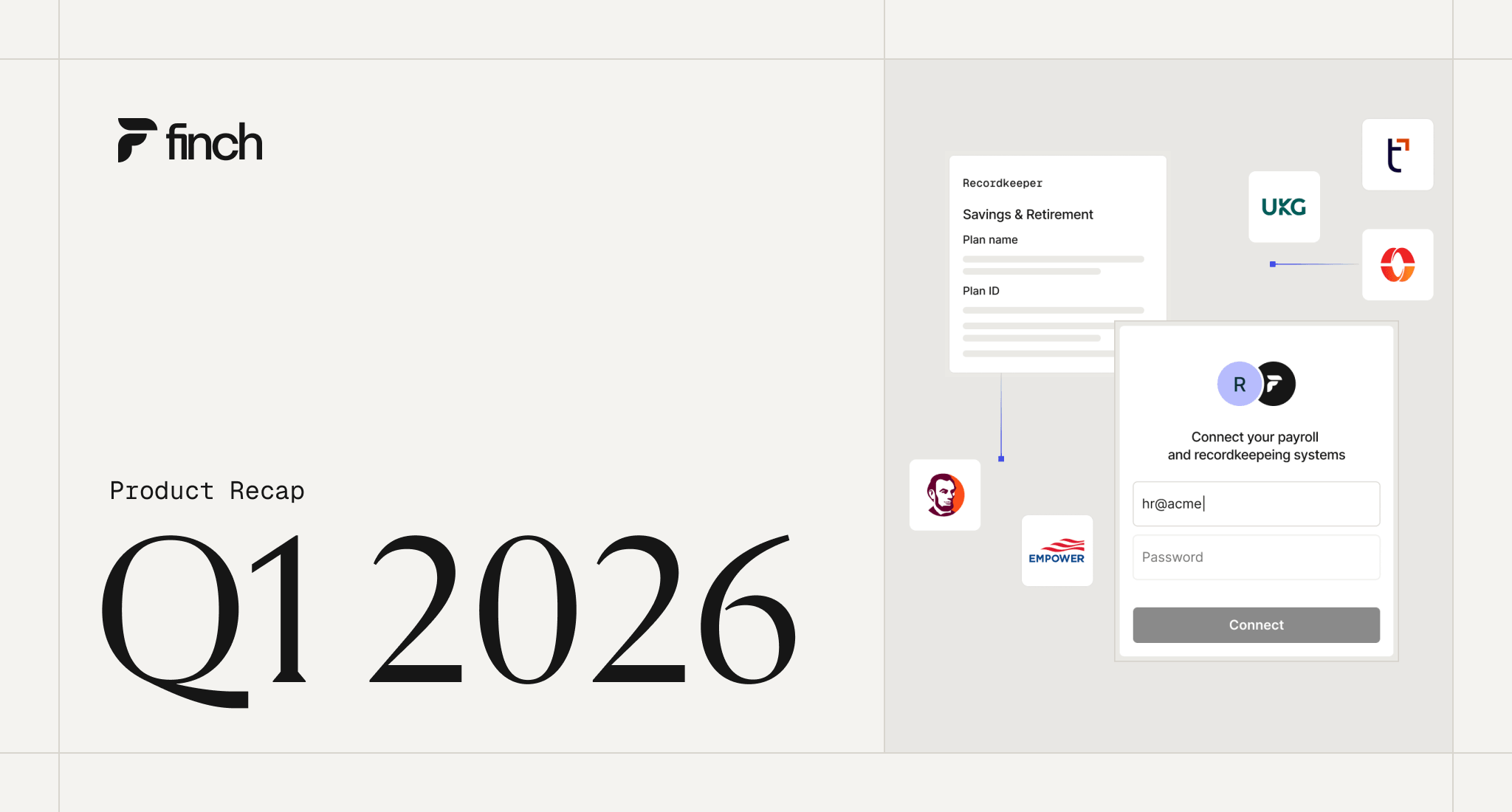

Q1 2026 Product Recap: Finch Recordkeeper, Deductions Mapping, and FLSA Status

Product

Finch

401(k) & Retirement

.png)

.png)

.png)

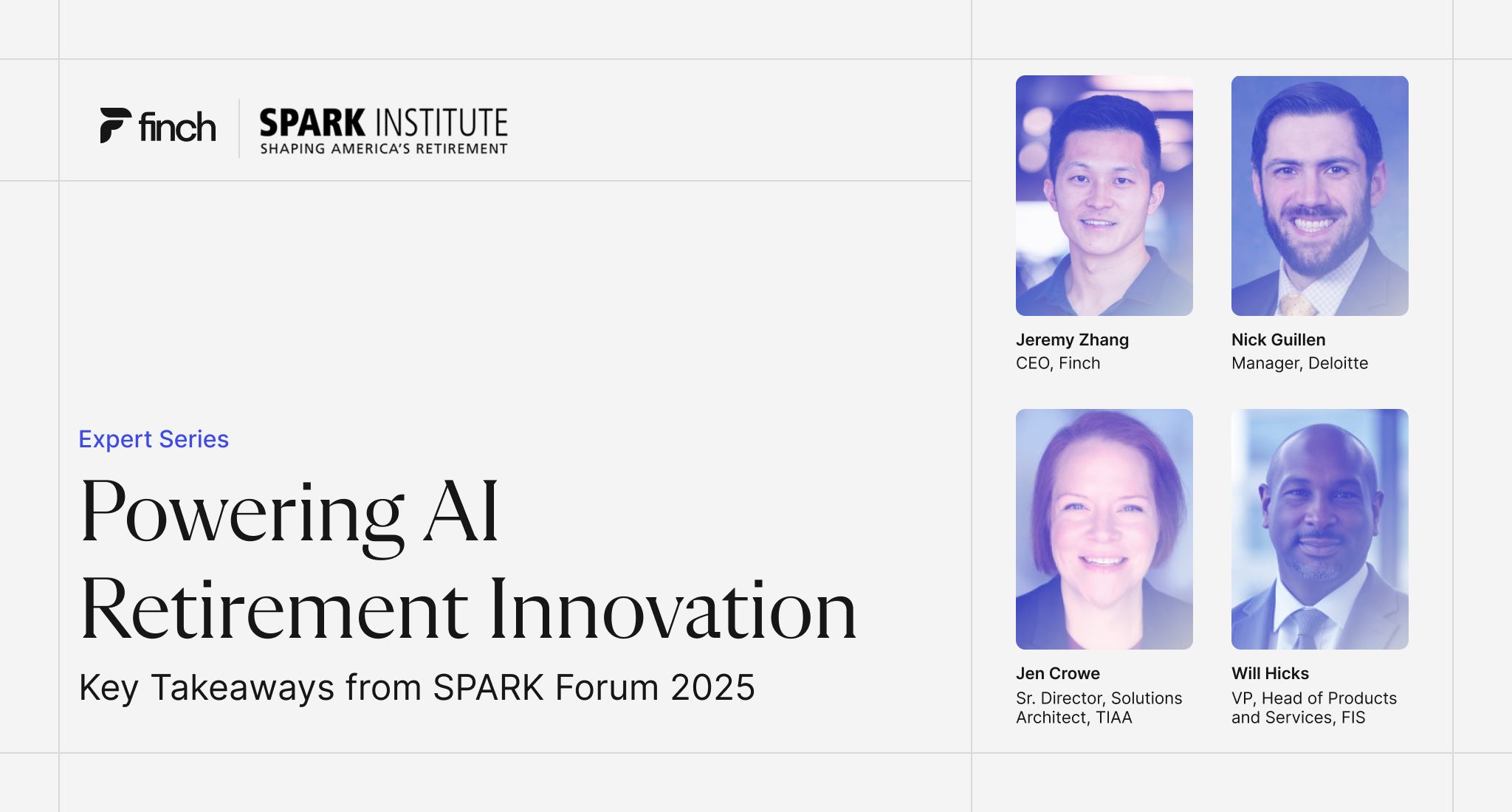

SPARK Forum 2025: Data, AI, and the Future of Compliance

401(k) & Retirement

Ecosystem

Compliance

Payroll

Powering AI Retirement Innovation: Key Takeaways from SPARK Forum 2025

401(k) & Retirement

Payroll

Benefits

Ecosystem

TIAA Teams Up with Finch to Optimize Data Integrity, Plan Outcomes

401(k) & Retirement

Payroll

Benefits

How to Choose the Right HR & Payroll Integration Partner [Free Buyer’s Guide]

API

Payroll

Compliance

Integration

Stax.ai Transforms TPA Operations with 80% Integration Adoption, Happier Sponsors

Case Study

401(k) & Retirement

Payroll

Partnership

How R&D Tax Credit Platforms Are Approaching the One Big Beautiful Bill Act

Finance

Integration

Payroll

Compliance