Sean Kelly is a seasoned retirement executive with more than 25 years of experience in the industry. Throughout his career, Sean has influenced every angle of 401(k) management, from plan administration to contribution oversight. He has served as the VP of Goldman Sachs RIA, VP of Retirement Services at Fulton Bank, and Director of Retirement Solutions at WisdomTree. Today, Sean is a Senior Growth Partner for the Pension Resource Institute and a retirement consultant.

It's no secret the retirement industry is undergoing a massive transformation. A series of concurrent factors—from SECURE 2.0 to the Millenial and growing Gen Z workforce—are pushing 401(k) recordkeepers to reconsider the ways they operate. Employers are also looking for a more integrated experience. They want retirement solutions that are tech-savvy and fit smoothly into their existing tech setup.

By now, you've probably heard of API integrations—the software connections that provide recordkeepers with direct, immediate access to sponsors' HRIS and payroll data. API-based payroll integrations are gaining popularity because they offer a faster and more scalable way to access employment data essential for seamless plan management. In the last few years, recordkeepers that have adopted API integrations over traditional data sharing methods like SFTP have minimized sponsor involvement in day-to-day administration and simplified the onboarding experience. Payroll APIs are fundamentally changing how recordkeepers operate.

In this article, we’ll discuss API integrations, why they are becoming a preferred choice for recordkeepers to access payroll data, and last but not least, how you can get started building your own integrations.

The role of payroll data in retirement

Needless to say, one of the core components of successful plan administration is ensuring that you’re working with complete and accurate payroll data. Payroll data is essential for plan administrators and recordkeepers to conduct participant eligibility checks and calculate deferral percentages and distributions.

Yet traditional methods of accessing sponsor’s payroll data, like Secure File Transfer Protocol (SFTP), are riddled with tedious and manual processes. It’s difficult for recordkeepers to get timely and accurate payroll and deduction data to run their operations smoothly. According to the IRS’s 401(k) Plan Fix-It Guide, most retirement plan errors result from inaccurate or incomplete payroll data made available to recordkeepers or plan administrators. And these errors have consequences. A simple mistake in recording plan contributions can lead to additional costs for sponsors like IRS/DOL penalties due to delayed or erroneous plan investments, along with additional time and resources needed to manually check and update the data.

With the explosion of payroll technology in recent years—from thousands of payroll tools to global employment platforms to embedded payroll—accessing sponsors’ payroll data has only become more complex. SFTP is falling short as the industry status quo, leading recordkeepers to look for new solutions.

Growing challenges for 401(k) recordkeepers

According to the Defined Contribution Recordkeeping Survey, recordkeepers currently administer services for over $10 trillion of defined contribution assets, with an increasing number of plans being added regularly. That equates to a massive volume of employee data handled by the industry.

Recordkeepers are starting to see that with new legislation driving larger and larger workloads for their Operations teams, SFTP is not the most optimal way to access mission-critical payroll data. As the industry evolves, SFTP will continue to fall short—but the impact on the recordkeepers that rely on it will only grow, making it far more difficult to:

- Support a large number of new sponsors, especially small and mid-sized businesses (SMBs) starting 401(k)s for the first time

- Streamline access to payroll data

- Maintain compliance

- Improve operational efficiency

Challenge 1: Supporting a large number of first-time SMB sponsors

Federal incentives under SECURE 2.0 and state mandates are driving a tidal wave of new SMB sponsors to the retirement market. These employers don’t have the robust HR departments of enterprise businesses to be involved with plan management. Recordkeepers that hope to earn their business must find ways to minimize sponsor involvement throughout the retirement plan cycle, reduce routine manual back-and-forth with the sponsor, and take more of the administrative duties off their customers’ plates. Using old-school methods like SFTP, where sponsors create and update payroll data files every pay cycle, will make it really difficult for 401(k) recordkeepers to handle a growing number of SMB sponsors.

Challenge 2: Streamlining access to payroll data

Traditionally, all payroll data has been locked in the sponsors’ HRIS and payroll systems. As more SMB sponsors start offering 401(k) plans thanks to SECURE 2.0, recordkeepers are finding themselves dealing with a larger pool of SMB payroll providers. It’s worth mentioning that the SMB payroll market is incredibly fragmented—there are nearly 6,000 providers in the US alone! On top of this, payroll data lacks standardization meaning each provider stores the same data in different formats under different fields.

File-based data sharing methods like SFTP require ongoing intervention from the sponsors for manually updating and uploading data files to the server. Plus, SFTP doesn’t account for the lack of standardization, meaning recordkeepers need to extract and standardize all the incoming data from sponsors into a format that works best for them. This adds further complexity and resource requirements for recordkeepers.

Challenge 3: Maintaining compliance

Payroll and other employment data are subject to compliance regulations that determine how these personal and sensitive data are collected, used, and stored. SECURE 2.0’s Sections 101, 125, and 603 stipulate sweeping eligibility changes, including mandated automatic enrollment, new eligibility for part-time employees, and updated rules for catch-up contributions—all of which make maintaining compliance harder than ever before.

Recordkeepers have to stay on top of employee eligibility data—when new employees can join plans, when existing employees can start making catch-up contributions, or when part-time workers reach the hours needed to join 401(k) and 403(b) plans. Any delay can cause recordkeepers to miss SLAs and face penalties.

Plus, the CSV or other flat files involved in SFTP are typically created by the sponsor on their end. This process is highly manual. When downloading, updating, and re-uploading data files, there are many opportunities for several Not in Good Order (NIGO) errors to be introduced to the system, such as improper data formatting and incorrect, missed, or delayed data entry.

Challenge 4: Improving operational efficiency

Taking on the work involved with supporting many small business plans will put a massive strain on recordkeepers' Operations teams. Scaling teams to keep up with manual work is not the most cost-effective solution, meaning recordkeepers are under pressure to improve operational efficiency and automate routine tasks involved in plan management—from automatic eligibility checks to automated deductions.

Other reasons why SFTP could be troublesome for recordkeepers

Besides those challenges, file-based systems can also create other problems for both recordkeepers and sponsors.

- SFTP can cause unnecessary delays. In case of a failed connection, you’re required to restart the process manually—from the beginning! No checkpoint restart is available with SFTP to restart the process from where you left off. Not only do sponsors have to re-upload files and restart the data-sharing process manually, there isn’t any automatic way in SFTP to recover from any sync failure. You need to have an army of developers and customer success resources ready to keep the sponsor experience seamless. With the criticality of the timeliness of payroll data, recordkeepers need a system that is reliable and requires a less extensive turnaround in case an outage occurs.

- SFTP involves a long, expensive set-up process. Lastly, building custom SFTP integrations that offer greater flexibility and control is time-consuming and resource-extensive, making it difficult to scale.

In short, SFTP is convenient for sharing a wide variety of files in large batches, but users are more likely to encounter errors related to the data’s formatting and accuracy. Plus, any file-based process like SFTP will still require a user to manually start the automation workflow, adding needless friction to the process.

As a result, recordkeepers are increasingly abandoning manual methods and opting for API integrations to avoid data mishaps. This is a smarter move because APIs are a more reliable, automated, and secure solution than SFTP.

{{retirement-1}}

Why should recordkeepers care about payroll APIs?

Application programming interfaces, or APIs, are tools that allow software applications to communicate and interact with each other. Having a live and continuous connection means that when data is updated in one system, it automatically updates in another. So, you're always working with the latest, most accurate version of the data.

Recordkeepers who often need fresh payroll data can really benefit from using API integrations.

- API integrations give recordkeepers instant and secure access to the employer's payroll systems in real time. This cuts down on errors and the amount of manual work both the sponsor and the recordkeeper have to do.

- Unlike manual processes involved in SFTP, APIs are more reliable because they directly fetch data from the employer’s source of truth—the HRIS and payroll tools they use.

- Unlike SFTP, APIs allow recordkeepers to request specific information they need instead of getting a huge load of data all at once. For example, with APIs, you can fetch the contribution information of a single employee instead of receiving the payroll details of the entire department or organization.

How are payroll integrations used in the retirement space?

Today, employers, in general, are much more aware of the benefits of integrations. A recent survey by Finch found that out of more than 1,000 HR professionals, 97% expect their systems to integrate with other tools, including the tools they use to manage employee retirement plans. So, integrations are not only an operational need for the recordkeepers but also a competitive advantage as they prepare to serve under the updated regulations in a larger retirement market.

To offer a more integrated sponsor experience, recordkeepers can connect their systems with the sponsors’ payroll tools through 180° or 360° integrations. While 180° integrations only send payroll data from the payroll system to the recordkeeper’s system, 360° integrations send data in both directions—meaning the recordkeeper can make direct changes to the payroll system without being forced to involve the sponsor. There are several benefits to using 360° payroll integrations as a recordkeeper, including:

- Simplified data access

- An improved sponsor experience

- The ability to automate routine tasks and more easily maintain compliance

Simplified data access

Payroll API integrations simplify payroll data collection and validation for recordkeepers, making sure all relevant data—such as sources of contributions, census data integrity, eligibility calculations, ongoing loan activities, and vesting confirmations—are correct, up-to-date, and obtained directly from the employer’s payroll systems. 401(k) payroll integrations allow recordkeepers to automatically pull sponsor data at any time in a standardized format—significantly increasing the efficiency of the data sharing process.

Improved sponsor experience

Payroll integrations allow recordkeepers to create a winning customer experience by reducing the plan sponsor’s day-to-day involvement, limiting their administrative responsibility, and eliminating constant back-and-forth with automated data transfer. When a sponsor grants their recordkeeper access to their HRIS and payroll data through a direct integration, the recordkeeper has full access to the standardized, relevant data they need to execute the plan, eliminating the typical onboarding pains. There’s no weeks-long process of identifying necessary data fields, creating standard PDI files, or quality control testing, so sponsors can onboard in a matter of hours or days—not weeks or months.

Automated routine tasks and better compliance

With access to sponsors’ census, demographic, and payroll data, enabled by 360° payroll API integrations, recordkeepers can automate many routine operational tasks, such as:

- Automatic enrollment of participants in plans as soon as they become eligible

- Auto-calculate the investment amount for each participant based on their deferral percentage, employer match, and earnings

- Update deferral changes directly in the sponsor’s payroll system instead of sending data back to the sponsor for manual updates

The benefit of automation trickles down from operational efficiency to improved compliance. Payroll integrations make legal and fiduciary compliance easier to maintain with proper and timely transmission of 401(k) contributions, automated eligibility checks, and automated deduction updates for their employees.

The emergence of unified employment APIs

APIs can provide immense value. However, APIs are usually specific to each software application and may require detailed knowledge of the application's functionality and the API's structure. In other words, building API-powered payroll integrations can be difficult, time-intensive, and costly. Finch’s research found that a single payroll integration can cost upwards of $187,500, and that doesn’t even include the ongoing maintenance costs or required partnership resources.

With the fragmentation of the SMB payroll market, it’s becoming increasingly harder for recordkeepers to build 1:1 integrations with each provider—rendering scaling integrations nearly impossible.

This is where tools like unified employment APIs are gaining popularity among recordkeepers, as they allow them to bypass the challenges of integrating multiple disparate payroll APIs with their systems, saving time and resources for more strategic initiatives.

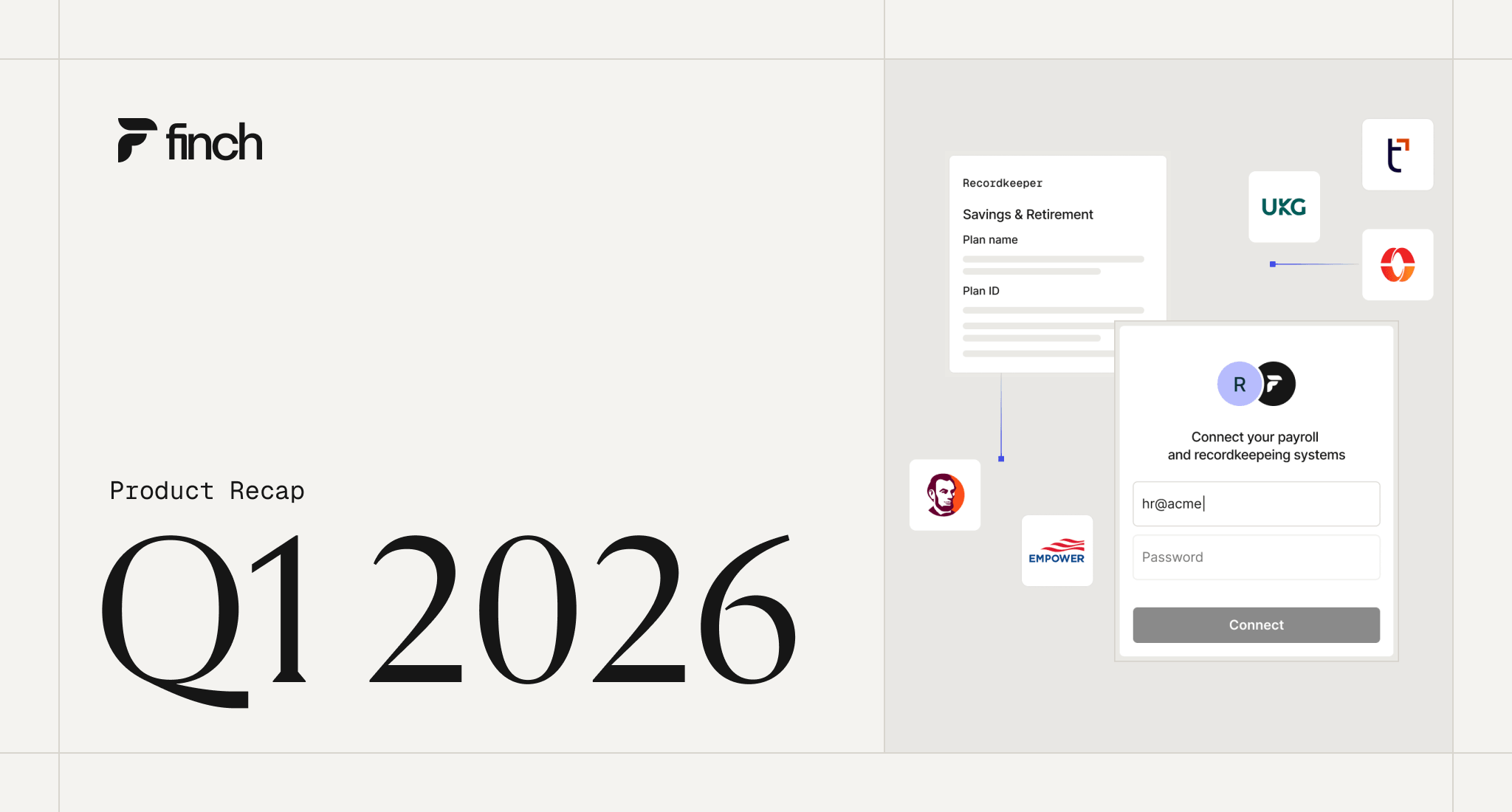

In simple words, a unified employment API adds a layer of technical connectivity that enables 401(k) recordkeepers to access data stored in the multiple payroll and HRIS systems their sponsors use—all through a single integration. As unified employment APIs are hyper-focused on the employment sector, the connections they provide not only offer greater stability, longevity, and data standardization, but also granular access to employment data, as deep as individual pay statements of employees.

By leveraging a unified employment API, recordkeepers can pull all the data they would typically need the sponsor to send manually over an SFTP server in real time and write changes back to the payroll system in a secure and timely manner.

The road ahead

The retirement industry is experiencing a significant shift and 401(k) recordkeepers and plan administrators are under tremendous pressure to adopt new technologies and reinvent their operations for higher efficiency. Payroll API integrations offer a pathway for recordkeepers to securely automate a significant portion of their day-to-day operations—from automatic enrollment in 401(k) plans to automating deduction updates back to the sponsor’s payroll systems.

However, API integrations, while convenient, aren’t simple. Each integration requires significant upfront and ongoing time and resource investment. This highlights the need for integration tools like Unified APIs that offer seamless access to payroll data from multiple systems. Just as Plaid revolutionized fintech connectivity, Finch’s Unified Employment API is setting the stage for a connected employment ecosystem where payroll data access is fast, secure, and programmable.

As we move toward a tech-forward retirement industry, API-based payroll integrations, along with tools like Finch, will become critical to shaping the future of plan administration. Learn more.