SECURE Act 2.0’s auto-enrollment and escalation rules

With the passage of the SECURE Act 2.0, automatically enrolling employees in sponsored retirement plans—and automatically increasing their contributions—is now a legal imperative. In response, retirement plan providers are implementing API technology to quickly and easily auto-enroll 401(k) and 403(b)participants and meet the new requirements.

In December 2022, the Securing a Strong Retirement Act (SECURE Act 2.0) was signed into law. Among the provisions outlined by SECURE 2.0 are new requirements for automatic plan enrollment and contribution escalation. Effective for plan years after December 31, 2024, they compel retirement plan providers to automatically enroll employees upon eligibility in new 401(k) and 403(b) plans and automatically increase the contributions of enrolled employees to that plan every year.

While these updates are exciting from a participation standpoint, the new requirements also come with the potential to create incredible administrative burdens especially in cases where employers are rapidly growing their workforce. In response, innovative retirement plan providers are implementing API solutions that integrate with employers’ HR information systems and payroll systems to ensure seamless SECURE 2.0 compliance. In this article, we explore the SECURE Act 2.0’s auto-enrollment and auto-escalation requirements plus the API technology that retirement plan providers are turning to make true automation a reality.

A SECURE Act 2.0 Summary

Building on the work of the Setting Every Community Up for Retirement Enhancement Act of 2019, SECURE Act 2.0 lays out widespread changes to the U.S. retirement system. The act is intended to make it more affordable for employers to sponsor retirement savings plans, and easier and more attractive for employees to participate.

The provisions of SECURE Act 2.0 include but aren’t limited to:

- An increase to the credit small businesses can receive for starting a pension plan

- Authorization for 403(b) plans to participate in multi-employer plans and pooled employer plans

- Higher “catch-up” contribution limits for individuals over age 50

- Permission to treat student loan payments as elective deferrals for purposes of matching contributions

- Permission for employers to incentives like gift cards to encourage plan participation among employees

- Allowance to withdraw emergency funds of up to $1,000 from retirement plans without text penalty

- An increase in the required minimum distribution age to 73

- The requirement that employers allow long-term, part-time workers to participate in sponsored retirement plans

In total, the plan details dozens of new rules and regulations. Retirement plan providers as well as employers should consult qualified legal counsel to understand the full extent of the impact of the law on their operations.

Read our new whitepaper: The Changing Retirement Landscape: How 401(1) Recordkeepers Can Thrive Under SECURE 2.0.

SECURE 2.0 auto-enrollment and auto-escalation

One of the most broadly impactful provisions of SECURE 2.0 is detailed under Section 101 of the law, which stipulates that new 401(k) and 403(b) plans must now automatically enroll employees upon eligibility. According to a summary issued by the Senate Committee on Finance, the decision to require auto-enrollment a matter of financial equity:

“One of the main reasons many Americans reach retirement age with little or no savings is that too few workers are offered an opportunity to save for retirement through their employers. However, even for those employees who are offered a retirement plan at work, many do not participate. But automatic enrollment in 401(k) plans…significantly increases participation. Since first defined and approved by the Treasury Department in 1998, automatic enrollment has boosted participation by eligible employees generally, and particularly for Black, Latinx, and lower-wage employees.”

Per SECURE 2.0, employees must be initially enrolled at a minimum of 3% of their gross pay but not more than 10%. Plans are also required to increase the distribution of enrolled employees each year by 1% until contribution reaches at least 10%, but not more than 15%.

Exceptions to the provisions include all current 401(k) and 403(b) plans, which are grandfathered into pre-SECURE 2.0 rules, as well as businesses with 10 or fewer employees, businesses under 3 years old, church plans, and government plans. Employees also have the right to opt out of enrollment or distribution escalation at any time.

What SECURE 2.0’s 401(k) auto-enrollment means for plan providers

Automatically enrolling all employees to a retirement plan upon eligibility is a significant undertaking. By SECURE 2.0’s definition, “automated” enrollment simply means enrolling those employees on an opt-out rather than an opt-in basis.

But that definition of automated doesn’t necessarily translate to a simpler, less manual process. A plan still needs to be notified of newly eligible employees and provided with the employee census data and payroll authorization it needs to process enrollment and manage recurring plan deductions. Without the right technology in place, employers and plans are forced to communicate all of this information by email, phone, spreadsheet, or secure file transfer. Not only is the back-and-forth time consuming, it increases the risk of error and noncompliance with SECURE 2.0’s provisions, and the potential of penalties and fine.. The hassle and risk only compounds in cases where employers are rapidly adding new employees.

How to auto-enroll 401(k) participants

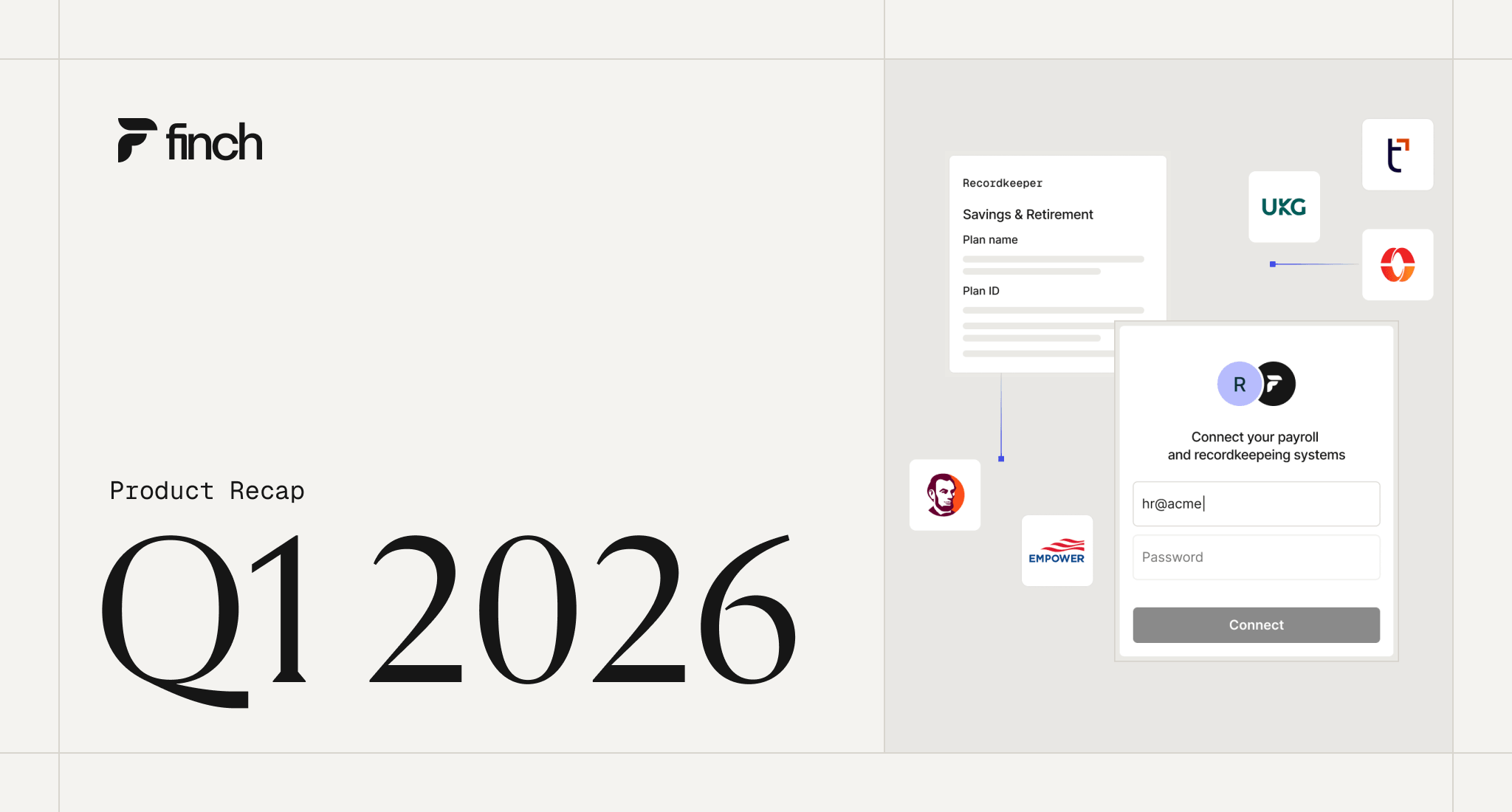

To avoid this drain of resources and to eliminate the risk of SECURE 2.0 noncompliance, true automation is critical. Retirement plan providers are now turning to API integrations with employers’ HR information and payroll systems to eliminate the manual steps historically needed to enroll employees and manage their deductions on an ongoing basis.

With an API integration, retirement plan providers have a direct, permissioned data connection to employment systems of record. This allows plans and employers to quickly and seamlessly exchange the data needed to enroll employees in 401(k) and 403(b) plans and manage their retirement deductions. What’s more, these data exchanges can be triggered by events without manual intervention, which means no person has to shoulder the responsibility of ensuring newly eligible employees get enrolled. The API integration takes care of it automatically in the truest sense of the word.

Consider this example:

- Company A is growing quickly and hires and onboards 7 new employees on the same day.

- As a matter of course, those employees are added by Company A to their HR information and payroll systems of record, which Company A’s 401(k) plan is integrated with via API.

- In turn, the 401(k) plan is automatically made aware that newly eligible employees have joined the company, which triggers an instant exchange of real-time data.

- With the information it retrieves from the HRIS, the 401(k) plan is able to automatically enroll all 7 employees. Via its direct payroll system connection, it is also able to make direct payroll changes to initiate recurring retirement contributions—no forms, emails, data entry, or spreadsheets required.

As a result, both the employer and the retirement plan provider save hours of administrative work and avoid delays to plan enrollment.

Implementing an API integration to auto-enroll participants and manage deductions

Retirement plan providers looking to enable HRIS and payroll system connectivity have a couple of options: build one-to-one integrations with all of the HRIS and payroll systems their customers use or partner with a turnkey, universal API that integrates with hundreds of HRIS and payroll systems at once.

Learn more about both approaches to HRIS and payroll integrations in our build vs. buy report.

The first approach offers plan providers ultimate control over their integration strategy but requires niche payroll expertise and a significant, ongoing investment of development resources. The second option turns over some of that control to a integrations partner but also comes with distinct advantages:

- More coverage, quicker—a universal API provides connectivity to many systems at once

- Faster go-to-market timeline—implementation takes weeks instead of months or more

- Fewer resources—the integrations provider does all of the heavy lifting, freeing up a plan’s internal team to focus on other priorities

- Worry-free maintenance—the integrations provider ensures the connections are working smoothly even as HRIS and payroll systems make updates

How Finch helps ensure SECURE 2.0 compliance

Finch makes it easy for retirement plan providers to integrate with 200+ HRIS and payroll systems with a single integration. Not only does our universal API enable the instant retrieval of real-time employee census data needed to automate 401(k) and 403(b) enrollment, it also allows plan providers to push changes directly to payroll. Using Finch’s Benefits endpoint, plan providers can initiate and manage pre-tax, post-tax, recurring, and one-time payroll deductions as a dollar amount or percentage of employees’ gross pay, ensuring easy compliance with the SECURE Act 2.0’s auto-escalation clause.

Meanwhile, the employer sponsoring the plan doesn’t have to lift a finger to upload deduction files or manually enter changes, saving them from hours of ongoing administrative work and avoiding countless potential human errors and potential fines.

Learn more about how retirement plan providers use Finch to build best-in-class customer experiences.

Get SECURE 2.0 compliant with Finch

The auto-enrollment and auto-escalation provisions of the SECURE Act 2.0 will drive retirement plan participation, but not without potential challenges and hurdles. Luckily, retirement plan providers who want to stay compliant while avoiding hassles and potential fines can leverage Finch’s universal HRIS and payroll system API to make true auto-enrollment and contributions management simple and secure. Register for a free test account to explore how to leverage Finch’s HRIS and payroll integrations today.