This post is part of Under the Hood, a series from Finch's product team on the real engineering and product challenges behind unifying payroll data at scale.

The benefits of unifying payroll data across the employment ecosystem are hard to overstate: faster and more reliable connectivity that allows clean, normalized data to flow between systems has enormous potential. Once data is unified and flowing, the logical next question is: what can you do with it?

At Finch, we started by solving the read side: pulling census and payroll data into a standardized format so that retirement platforms, benefits administrators, and other employment software could access it reliably. But our customers don't just need to read data; they need to act on it, whether by enrolling participants, managing deductions, or pushing changes back to payroll systems. That's where the complexity compounds.

When we launched our Deductions product, we gave our customers the ability to make changes in provider systems via a unified interface. Now, we're taking that capability further to power full end-to-end workflows with downstream integrations and deeper write capabilities, and connecting the larger benefits ecosystem.

Here's how we believe we’ll create a more connected ecosystem.

How it started: from read-only to read-write

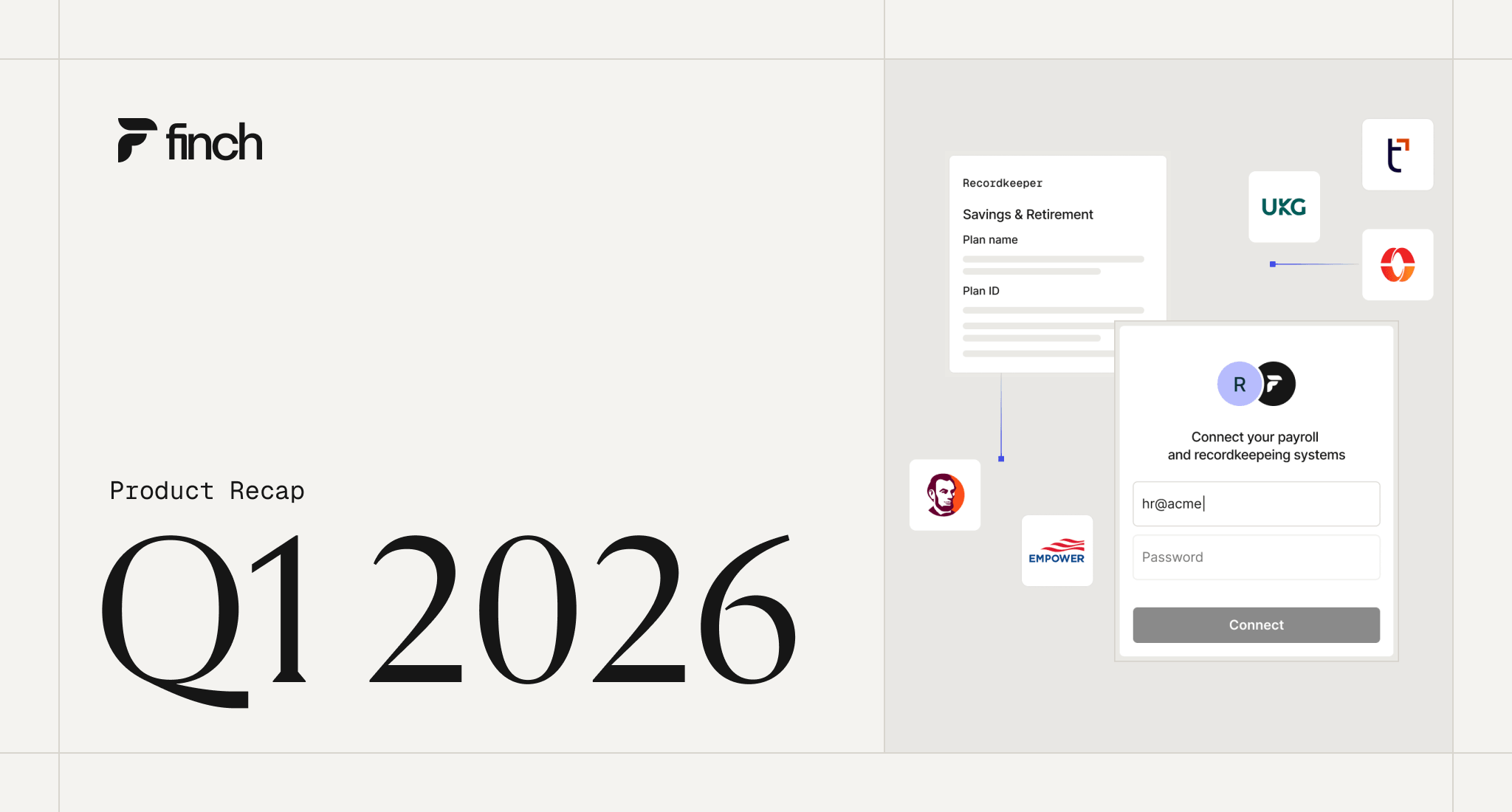

Finch's initial value proposition centered on the read side. For any benefits provider, the first need was access to the employee’s data: who works at this company, what do they earn, and what benefits are they enrolled in? We solved that by pulling data from payroll providers and delivering it in a standardized format through our unified API.

But the product needed to do more. Retirement recordkeepers need to create and update retirement contributions in the payroll system; benefits administrators need to push benefits changes when an employee's plan changes. The value of a unified data layer increases dramatically when it can write as well as read.

That's what our Deductions product introduced. Customers could now create benefits, enroll employees, and manage deductions programmatically through the same unified API they were already using for read operations. For the first time, benefits providers could create benefits in the employer’s payroll system and programmatically manage them.

This was a big step forward, but it also surfaced a new class of problems. Writing data back to payroll systems means dealing with the full complexity of each system—and how each employer has configured them.

Where we are: powering end-to-end workflows

Today, Finch is moving beyond individual API operations toward powering complete workflows across the benefits ecosystem. That means solving three interconnected challenges at once.

Connecting with downstream platforms

The benefits ecosystem runs on infrastructure that has been in place for decades. For example, retirement recordkeepers and insurance providers have established systems and data formats that their operations depend on. Our goal isn’t to replace that infrastructure, but to integrate with it.

In practice, this means Finch connects with downstream platforms and implements flexible data delivery methods. The key principle we’re operating under is that customers shouldn't have to rip out existing infrastructure to use Finch. We’ll meet the ecosystem where it is.

Standardizing provider differences with employer input

This is the hardest piece. Employee and employer contributions (401(k) contributions, health insurance premiums, HSA contributions, loan repayments, and so on) are the most inconsistently represented data types in payroll. But the inconsistency isn't just at the provider level; it compounds at the employer level.

Every employer configures their payroll system differently. Take the example of a retirement plan. Two employers on the same provider might label the same 401(k) contribution differently: one as a custom code tied to their plan administrator's naming convention, another using the provider's default. An employer might split what looks like a single contribution type into multiple line items to track Roth and pre-tax contributions separately, or bundle distinct contributions under a single catch-all code. The configurations reflect real differences in how each employer's benefits are structured, and there's no universal standard.

You can't solve this with provider-level logic alone. Even if you've perfectly normalized how a given provider represents a 401(k) deduction, you still need to know what this specific employer means by the code they've configured.

Finch's approach treats this as a collaboration between the platform and the employer. We built a mapping infrastructure that lets employers label their own payroll items across earnings, deductions, and contributions through our dashboard or API. Each label set is scoped to the downstream system it's feeding, because a recordkeeper has different requirements than a benefits administrator. Finch provides the structure, surfaces the data, and offers defaults where we can infer them. The employer validates the specifics.

The mapping is the connective tissue that makes the end-to-end workflow function. Without it, you're guessing at what an employer's codes mean, and in benefits, guessing means misallocated contributions, failed compliance tests, and enrollment errors that are expensive to unwind.

Ultimately, employers know what works best for their organization—our approach creates a standardization layer on top of that.

Flexible data delivery for the right use cases

Different use cases demand different delivery methods. A retirement recordkeeper processing contributions on a payroll cycle might need file-based exports with specific column formats, delivered automatically. A benefits platform managing real-time enrollment changes may need API access with on-demand delivery. And a TPA running compliance testing needs bulk data on a different cadence entirely.

Finch supports both file-based and API-based delivery, with automatic and on-demand options, so that each customer's integration matches their actual workflow. The flexibility matters because the value of unified data disappears if it can't reach the systems that need it in the format they expect.

Where we're going: a more connected ecosystem

Everything we've built so far—data unification, write-back capabilities, mapping, downstream connectivity—has focused on specific use cases: retirement, insurance, ICHRA. But the underlying infrastructure points toward something larger.

Consider what becomes possible with a unified source of truth for employers' and employees' benefits across the entire ecosystem. Individuals could receive more personalized financial guidance, employers would have more power to evaluate and switch between benefit providers based on what's best for their workforce, and benefit providers themselves could serve their clients more effectively with better data about what's already in place.

That's the trajectory. Finch is moving from unifying data to unifying workflows to, eventually, creating a more holistic view of the employer across the entire employment ecosystem. Getting there depends on getting each foundational layer right, and I’m incredibly excited about the implications of a more connected ecosystem.

You can learn more about Finch's capabilities in our developer docs, or sign up for our sandbox to explore the API for yourself.