Earlier this year, TIAA teamed up with Finch to integrate secure, permissioned payroll connectivity into their plan administration platform. With 360-degree payroll connectivity, TIAA will enable streamlined employer onboarding, automate deductions management, and optimize data integrity by collecting information directly from the sponsors’ sources of truth.

TIAA Retirement Solutions COO Raymond Bellucci recently sat down with Finch CEO Jeremy Zhang to share his perspective on the changing retirement landscape, TIAA’s vision to broaden access to savings plans and encourage earlier participation, and the role of technology in helping to drive better outcomes for participants.

Q&A with COO of TIAA Retirement Solutions Raymond Bellucci

You started your TIAA career as a high school student working in the mail room and have held 17 different roles since joining the company full-time in 1983. How has this breadth of experience shaped your view of the retirement industry and your work at TIAA?

I'm a product of the New York City public school system, and in high school they had a program called Cooperative Education, where students would alternate weeks going to school and working for a company. I was assigned to this company, TIAA-CREF at the time, back in 1981.

It was a phenomenal program for kids who didn't know whether or not they'd be able to go to college, and TIAA was a fantastic opportunity. Over the last 42+ years with the company, I've been really fortunate. I've worked for six CEOs at TIAA, each of whom has given me an opportunity to learn more about the marketplace and the industry. I've been able to work on the product side of our organization and lead technology teams, but the one constant over my four decades has been our clients. Our mission at TIAA is to serve those who serve others, and it's an incredibly motivating, inspiring mission that hasn't wavered in the time I've been here. If anything, we're more committed to that mission now than ever.

Which of your 17 roles did you enjoy the most, and which was the hardest?

The hardest one and the one I enjoy the most is the role I'm in, Chief Operating Officer for the Retirement Solutions business; but I say that almost jokingly.

For the first 12 years of my career, I worked on the institutional and operational side of the business, and then in the mid-1990s, I had the opportunity to work on the individual side of the business, counseling participants. And that’s where you really begin to see TIAA’s mission come to life.

We were founded by Andrew Carnegie, whose dream was that educators would retire with dignity and wouldn’t run out of money. You don’t really see that on the operations side — you see the transactions, but you don’t get to see the impact you have on people’s lives. When I sat down with a participant and saw how much they trusted us, it really was a moment where I thought, “Okay, this isn’t a job for me anymore. I could make a career out of this.”

I know the impact on employees is incredibly important to this industry, and especially to TIAA. About 55 million Americans still don’t have access to a retirement plan at work. What’s your vision for how TIAA can broaden access to retirement plans and encourage more people to save?

It's a great question. We believe we can turn that around. What really propels TIAA forward is our belief in in-plan guaranteed lifetime income options, which is our unique way of approaching the retirement crisis.

We’ve made our Secure Income Accounts available to the general public through other retirement plans and other recordkeepers. So we believe that we can help solve the retirement crisis in America through this solution that we’ve been offering for 107 years, and by making it more broadly accessible.

When the SECURE Act 1.0 passed in December 2019, it gave certain protections to plan annuities, to lifetime income products within a retirement plan. And I think that’s recognition that we have the opportunity to do more, and we need to have solutions in retirement plans that protect workers into the future.

The TIAA Institute recently published research that found nearly ⅔ of Americans feel that retiring “on-time” is unattainable and 20% of adults currently aren’t saving for retirement. What do you think is the core issue underlying this problem?

Life! Retirement is one of those things that always seems to be out in the future somewhere. Our CEO Thasunda Brown Duckett has said when you join a company where there’s a retirement plan available, participate. I know as a younger employee, the first thing you’re worried about is paying your bills, but even if you can only save 1% to start, it’s so important to start saving what you can as early as you can. It’s about choices, and sometimes it’s about delayed gratification.

If you're mid-career or older, try to catch up. It's never too late to start saving. It's never too late to look at the future. As a financial consultant, I've sat down with participants who've wanted to retire in two years and I told them you might need to wait a little bit longer. And that’s okay, because waiting a little bit longer is protecting your future.

You mentioned the industry has seen a lot of regulatory changes, particularly through the SECURE Acts. We’re also seeing a lot of states mandating employers sponsor a retirement plan, and emerging technology like AI and other infrastructure products. From your perspective, how have these changes — both on the regulatory side and the technology side — impacted how you view operating with efficiency at TIAA?

Whether it’s state-mandated IRAs or Trump Accounts, any legislation that starts the conversation to encourage young workers to save for retirement benefits us all.

On average, 80% of participants default into their retirement plan. That means they’re not really choosing to participate, they’re defaulting into it. And that’s what the Pension Protection Act was all about: protecting employees who don't make an investment decision. Things like auto-enrollment are for those employees who aren’t really engaged with their plan.

The best way to protect the unengaged employee is to get them to engage. That’s why at TIAA, we’re so focused on the customer experience and creating a compelling reason for employees to engage with us, with their retirement plan. So we’re supportive of any legislation that gets people participating in the conversation.

But I think the biggest impact is technology, because it's inherently making us more efficient: transaction processing is faster better, and AI is giving us the ability to more deeply understand what our clients need.

TIAA recently started working with Finch to enable payroll connectivity, which we’re really excited about. Can you tell me more about the opportunity you’re creating and your decision to work with Finch?

Absolutely, and we're as excited as you are about working together.

For years, we've been working with plan sponsors and plan administrators and third parties to receive more comprehensive data as the recordkeeper.

Having a capability like the one we're working on with Finch will give us the ability to engage directly with the payroll system, which is the system of record, or the source of truth.

So having a capability like Finch has and working with TIAA to have that 360 degree exchange of data directly with the payroll system gives us the fullest, most complete, and — most importantly — the most precise data. Because if the data you're using for payroll is matching exactly, then we know that our books and records are as up to date as the plan sponsors’.

And that's a big deal. We want to ensure optimal data as we exchange files. And enhancing the data allows us to enhance the quality of the outcome for the plan participant and the ability to look at that plan participant more holistically, because we know more than just the amount they're contributing each pay period or each month.

97% of HR professionals say it’s important for your app to integrate with their employment systems

Learn more in our State of Employment Technology report ->

97% of HR professionals say it’s important for your app to integrate with their employment systems

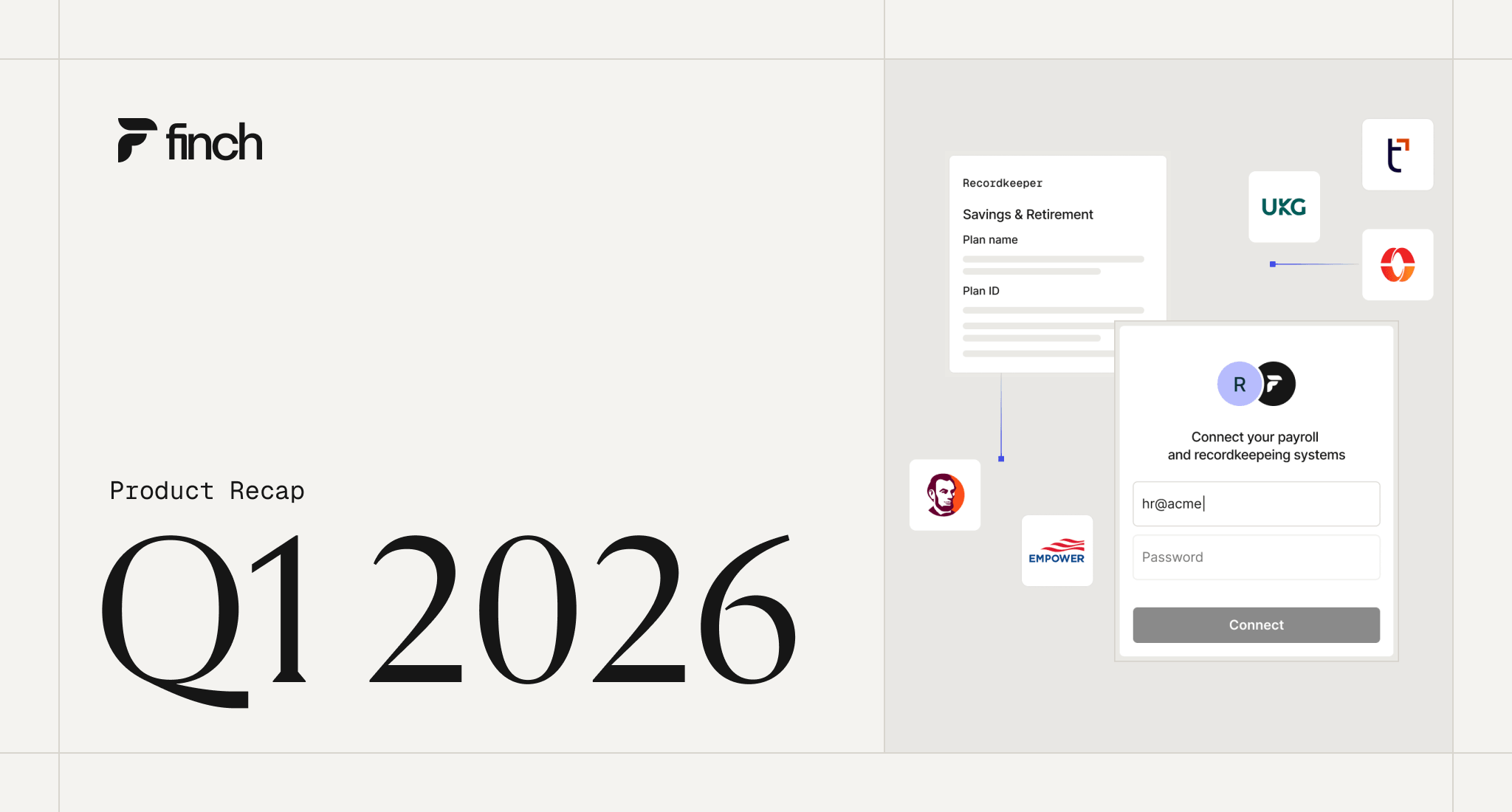

Payroll Integrations Made for Retirement